IMPORTANT DISCLAIMER: This content is for informational purposes only and does not constitute financial, legal, or retirement planning advice. Federal employees must conduct their own research and consult with qualified professionals before making retirement decisions. The information presented here is subject to change based on federal regulations and OPM guidance.

Federal employees covered under the Federal Employees Retirement System (FERS) who separate from service before reaching standard retirement eligibility face critical decisions regarding their accumulated retirement benefits. Two distinct options exist: deferred retirement and postponed retirement. These pathways carry significantly different eligibility requirements, benefit structures, and long-term financial implications that require careful analysis and professional consultation. For personalized federal retirement analysis and strategic planning consultation, federal employees may schedule appointments through our Benefits Review service.

Understanding Deferred Retirement Under FERS

Deferred retirement represents a pathway for federal employees who terminate employment before meeting immediate retirement eligibility but have accumulated the minimum required service credit. This option allows former employees to claim retirement benefits at a future date while maintaining their investment in the FERS system.

Eligibility Requirements for Deferred Retirement

CRITICAL REQUIREMENT NOTICE: All eligibility criteria must be satisfied without exception.

To qualify for deferred retirement benefits, separated federal employees must meet the following mandatory conditions:

- Minimum Service Requirement: Complete at least five (5) years of creditable civilian service under FERS

- Contribution Retention: Leave all retirement contributions within the FERS system without requesting refund upon separation

- Non-Immediate Retirement Status: Must not qualify for immediate retirement benefits at time of separation

- System Compliance: Maintain compliance with all OPM regulations regarding deferred benefits

For complete eligibility verification and current requirements, federal employees should reference official guidance at OPM.gov.

Deferred Retirement Benefit Commencement

NOTICE: Benefit timing is strictly governed by federal regulations and cannot be modified based on individual circumstances.

Deferred retirement annuities commence under specific age and service combinations:

- Age 62 with 5 Years: Unreduced annuity available at age 62 with minimum 5 years creditable service

- Age 60 with 20 Years: Unreduced annuity available at age 60 with 20 years creditable service

- MRA with 30 Years: Unreduced annuity available at Minimum Retirement Age (MRA) with 30 years creditable service

WARNING: Early commencement of deferred benefits may result in permanent reduction of monthly annuity payments.

Significant Limitations of Deferred Retirement

IMPORTANT LOSS OF BENEFITS NOTICE: Deferred retirees forfeit critical federal employee benefits upon separation.

Employees electing deferred retirement face the following permanent benefit losses:

- Federal Employees Health Benefits (FEHB): Complete loss of health insurance coverage upon separation with no opportunity for reenrollment when annuity begins

- Federal Employees Group Life Insurance (FEGLI): Termination of life insurance coverage upon separation

- Special Retirement Supplement (SRS): Permanent ineligibility for the supplement that approximates Social Security benefits for FERS retirees under age 62

- Immediate Coverage Gap: No federal health or life insurance protection during the period between separation and annuity commencement

Postponed Retirement: The MRA+10 Strategy

Postponed retirement serves as an exclusive FERS option designed for employees who meet MRA+10 eligibility requirements but choose to delay benefit commencement to reduce or eliminate age-related penalty reductions.

Eligibility Requirements for Postponed Retirement

STRICT ELIGIBILITY NOTICE: Postponed retirement is available only under specific circumstances.

Postponed retirement eligibility requires:

- FERS System Coverage: Available exclusively to FERS-covered employees

- MRA+10 Qualification: Must satisfy Minimum Retirement Age plus 10 years of service requirements at separation

- Contribution Retention: Must retain all retirement contributions within the system

- Strategic Election: Must formally elect to postpone annuity commencement beyond separation date

Age Penalty Reduction Strategy

FINANCIAL IMPACT WARNING: Age penalties result in permanent monthly annuity reductions that compound over the lifetime of retirement.

Under MRA+10 provisions, retirement benefits suffer a five percent (5%) annual reduction for each year the employee falls short of age 62 or the age required for unreduced benefits. Postponed retirement allows strategic delay of benefit commencement to minimize or eliminate these penalty reductions.

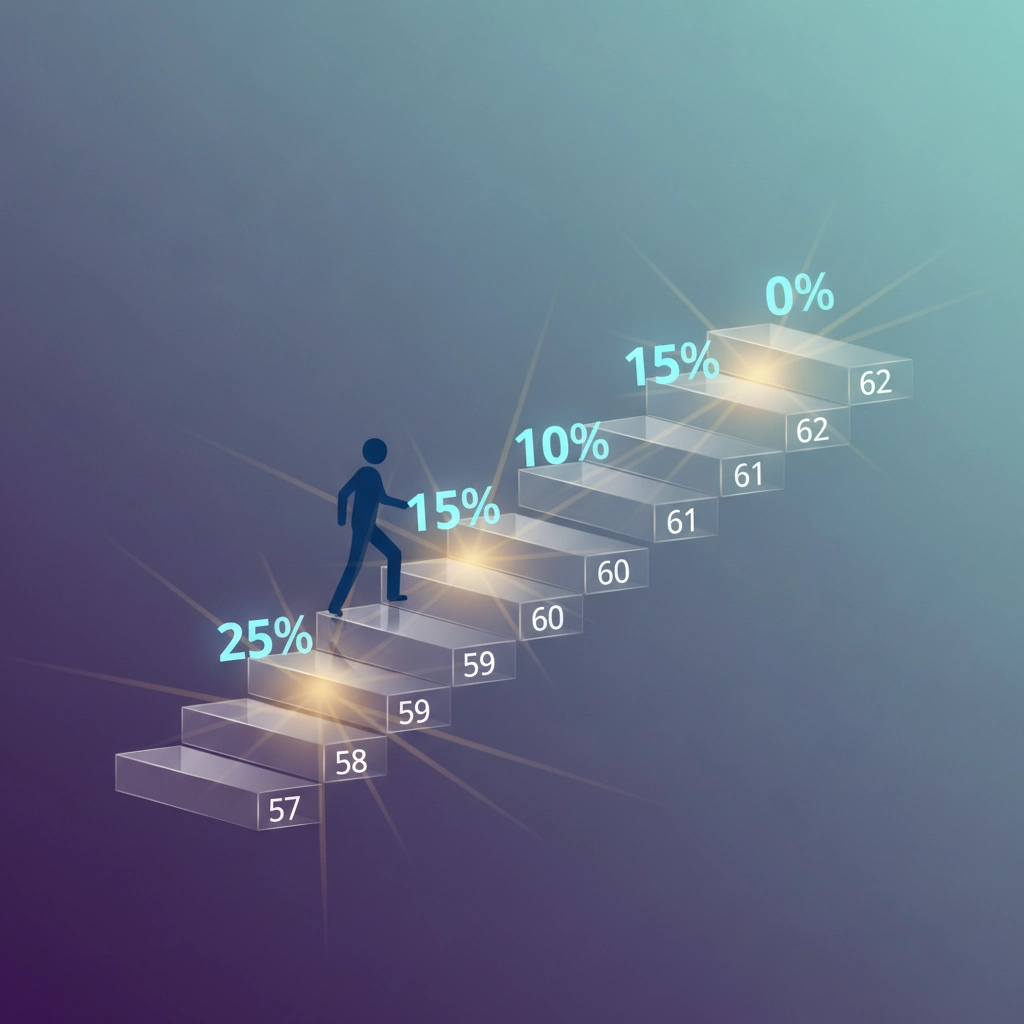

Example Calculation for Educational Purposes Only:

- Employee separates at MRA (57) with 15 years service

- Five-year gap to age 62 results in 25% permanent annuity reduction

- Postponing commencement to age 60 reduces penalty to 10%

- Postponing to age 62 eliminates penalty entirely

DISCLAIMER: This example is for illustrative purposes only. Individual calculations vary based on specific circumstances and current federal regulations.

Postponed Retirement Benefit Considerations

BENEFIT RESTORATION NOTICE: Certain benefits may be available for postponed retirees that are not available for deferred retirees.

Postponed retirement provides the following benefit considerations:

- FEHB Reinstatement: Potential opportunity to reinstate Federal Employees Health Benefits coverage when annuity commencement begins

- FEGLI Considerations: Life insurance reinstatement subject to program rules and medical underwriting requirements

- SRS Ineligibility: No eligibility for Special Retirement Supplement regardless of postponement strategy

- Social Security Coordination: Standard Social Security benefits available at appropriate ages

- COLA Eligibility: Cost-of-Living Adjustments apply to civil service benefits beginning at age 62

Comparative Analysis: Deferred vs. Postponed Retirement

ANALYSIS NOTICE: The following comparison is for informational purposes only and does not constitute a recommendation for either option.

2026 Planning Considerations

CURRENT YEAR NOTICE: The following information reflects conditions for calendar year 2026 and is subject to change based on federal determinations.

Cost-of-Living Adjustments for 2026

The 2026 FERS Cost-of-Living Adjustment has been established at 2.0 percent for existing retirees. This adjustment serves as a benchmark for understanding benefit growth patterns but does not directly impact deferred or postponed retirement calculations until benefits commence.

Strategic Separation Timing for 2026

TIMING WARNING: Improper separation timing can result in loss of leave benefits and create gaps in retirement income.

Federal employees planning separation in 2026 should consider the following optimal dates:

- End-of-Month Separations: Retiring at month-end prevents loss of accrued sick and annual leave

- Pay Period Alignment: Separation dates aligned with pay period endings (May 30, June 27, October 31, November 30, 2026) ensure seamless transition to retirement annuity without income gaps

For current separation guidance and optimal timing strategies, consult official resources at OMP.gov.

Risk Assessment and Professional Consultation Requirements

MANDATORY CONSULTATION NOTICE: Federal retirement decisions carry long-term financial implications that require professional analysis.

Both deferred and postponed retirement involve complex calculations and permanent benefit elections that significantly impact lifetime retirement security. The following risk factors require careful evaluation:

Financial Risk Considerations

- Healthcare Coverage Gaps: Loss of FEHB coverage creates immediate health insurance needs

- Income Replacement Analysis: Benefit timing affects total lifetime income calculations

- Longevity Projections: Life expectancy estimates impact optimal claiming strategies

- Inflation Protection: COLA timing and coverage varies between options

- Survivor Benefit Elections: Spousal protection requires specific election timing

Professional Consultation Requirements

DO YOUR OWN RESEARCH NOTICE: This information does not substitute for personalized professional consultation.

Federal employees must:

- Conduct independent research using official OPM resources

- Consult with qualified financial professionals familiar with federal benefits

- Analyze personal financial circumstances and retirement goals

- Review all legal and regulatory requirements before making elections

- Seek independent verification of all benefit calculations and projections

NO INVESTMENT ADVICE DISCLAIMER: This content does not provide investment recommendations or guarantee future benefit amounts.

Implementation and Next Steps

ACTION REQUIRED NOTICE: Federal employees must take specific actions to implement deferred or postponed retirement strategies.

Mandatory Implementation Steps

- Official Documentation Review: Obtain current benefit statements and service credit verification from OPM

- Regulatory Compliance: Ensure all separation procedures comply with agency and OPM requirements

- Election Timing: Submit required forms and elections within specified deadlines

- Professional Consultation: Engage qualified federal retirement specialists for personalized analysis

- Ongoing Monitoring: Maintain awareness of regulatory changes that may affect benefit calculations

Professional Benefits Review Scheduling

CONSULTATION RECOMMENDATION: Federal employees should schedule comprehensive benefits review appointments to analyze individual circumstances.

For personalized federal retirement analysis and strategic planning consultation, federal employees may schedule appointments through our Benefits Review service. Professional consultation provides individualized analysis of deferred versus postponed retirement options based on specific service credit, financial goals, and personal circumstances.

FINAL DISCLAIMER: All federal retirement decisions should be based on current OPM regulations, individual financial analysis, and professional consultation. This content is for informational purposes only and does not guarantee specific benefit amounts or outcomes.